This report from the TIAA Institute and Nuveen examines how 401(k) participants approach retirement withdrawal planning and measures their retirement fluency and longevity literacy, the foundational knowledge needed to make sound retirement decisions.

Summary

While 71% of 401(k) participants have thought at least some about converting savings to retirement income, only 22% have thought about it deeply, and that gap matters. Participants who engage more thoroughly are more likely to use plan-provided tools, rate those tools highly, and feel confident about making withdrawal decisions. Yet knowledge gaps remain a serious barrier to addressing a wider range of retirement planning issues: participants correctly answered only 5 of 15 retirement fluency questions, on average, with the lowest scores in long-term care and retirement withdrawals. Longevity literacy is equally concerning, only 33% correctly estimated life expectancy after age 65, while 44% underestimated it, risking plans built on retirement horizons that are simply too short.

Key Insights

- Withdrawal planning is shallow. About 70% of 401(k) participants have thought a lot about how to convert savings to retirement income, but only 22% have thought a lot about it including just 19% of late-career participants closest to retirement.

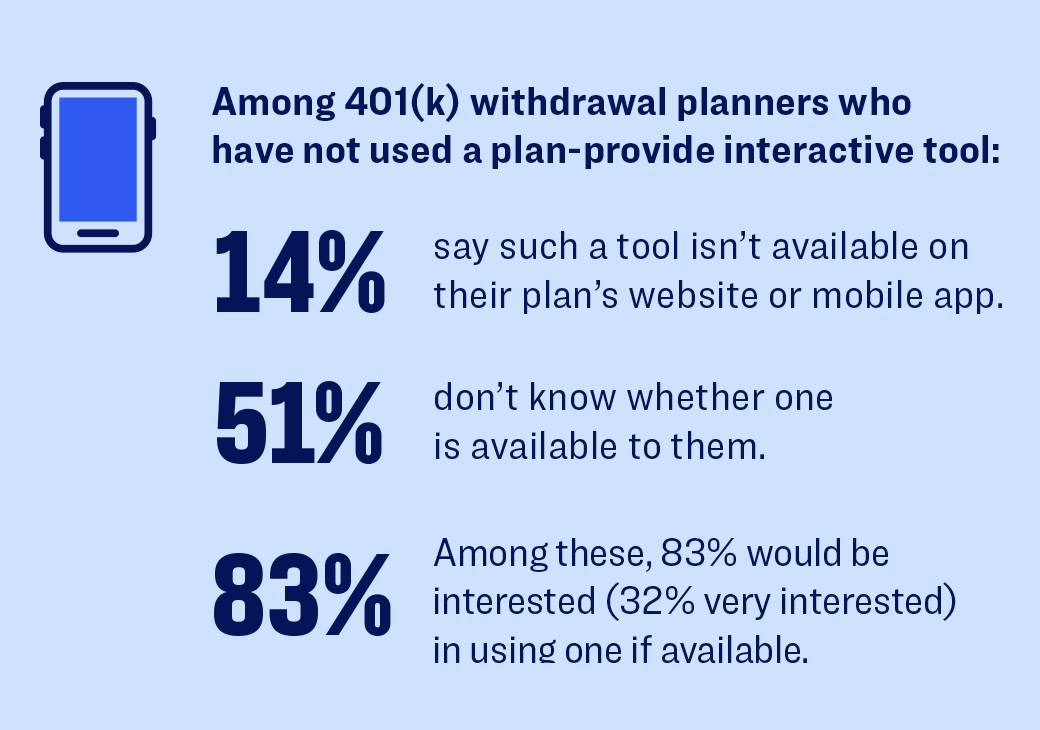

- Nine-in-ten withdrawal planners think it’s important for employers to provide resources to help employees determine how best to make retirement withdrawals, while 49% feel it’s an employer’s responsibility to provide such guidance.Using both interactive and noninteractive resources boosts confidence significantly. Among participants who used both types of tools, 53% are very confident they will choose the best withdrawal strategy, compared to just 28% of those who used neither.

- Retirement fluency is critically low. Participants answered only 32% of retirement fluency questions correctly on average, with 52% answering fewer than one-third correctly. Knowledge gaps were deepest in long-term care (27% correct) and retirement withdrawals (26% correct).

- Most participants underestimate how long individuals tend to live after reaching age 65. Only 33% of participants correctly answered the longevity literacy question, while 44% underestimated average life expectancy at age 65, leaving them at greater risk of running short of money in retirement.