This TIAA Institute research examines how nonprofit sector employees make contribution location decisions — specifically, whether to direct retirement savings to traditional pre-tax or Roth accounts. The study explores how participant characteristics, plan design features, and behavioral inertia shape these decisions and their implications for retirement security.

Summary

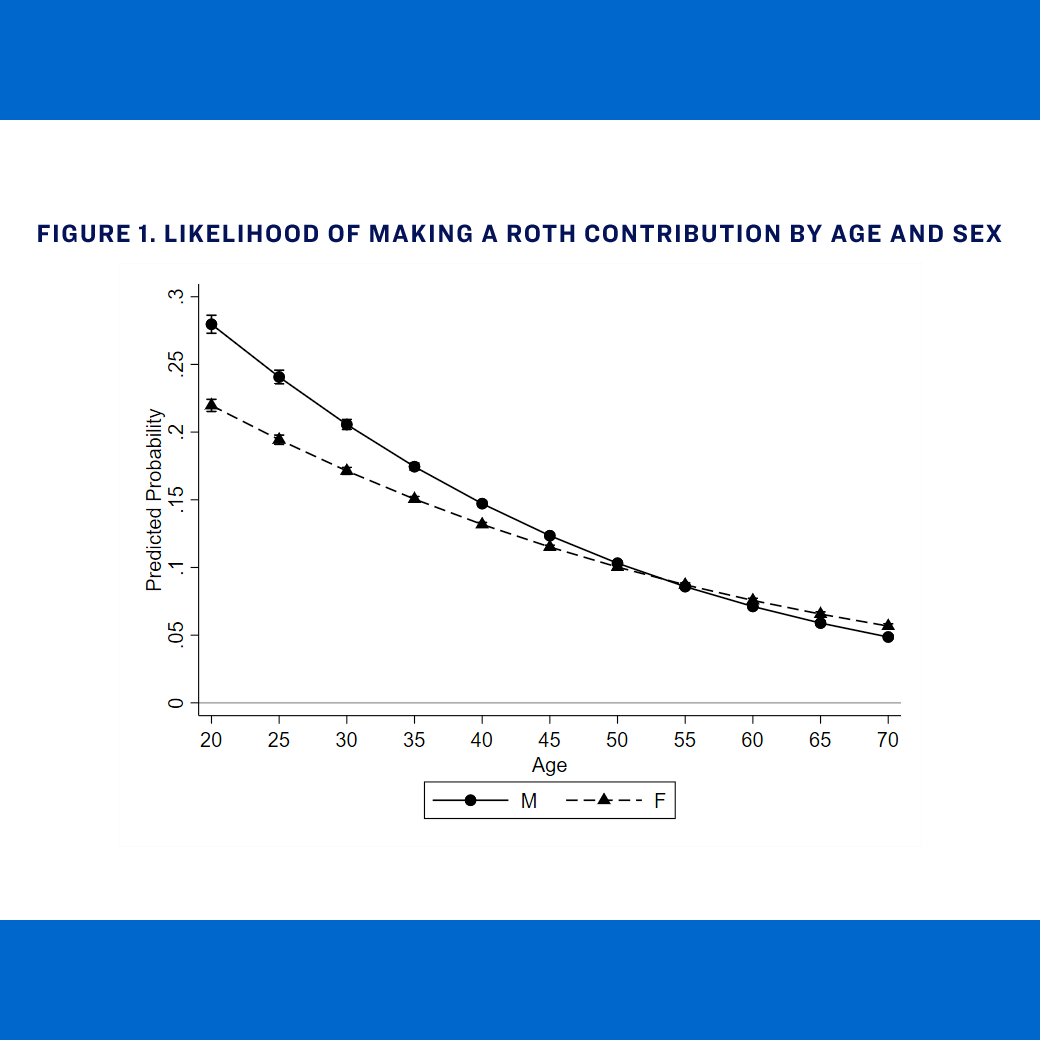

Among contributing participants with access to a Roth account, 12% chose to use one. Younger workers and those who made active investment elections were significantly more likely to direct contributions to Roth accounts, while participants who defaulted into plan investment options were more likely to use pre-tax accounts. Workers subject to mandatory employee contributions were notably more likely to make Roth contributions. Among those who elected Roth contributions, most used Roth accounts exclusively for their employee contributions. Using an event study, workers who joined a plan before a Roth option was introduced were nearly 10 percentage points less likely to use Roth accounts than those who joined after, and this trend did not reduce across time.

Key Insights

- Only 12% of participants with access to a Roth account option used it, and most of those participants use Roth account exclusively for their employee contributions.

- Younger participants and those who made active investment elections were significantly more likely to contribute to Roth accounts.

- Whether or not participants were in plans subject to mandatory contributions significantly impacts contribution location and savings decisions because mandatory contributions are on a pre-tax deferral basis.

- Participants who enrolled in their plan before a Roth option was introduced were nearly 10 percentage points less likely to use Roth accounts than those who enrolled after the option became available, and this gap did not meaningfully close over time, indicating a large inertia effect.