In 2023, 9% of U.S. retirees were underbanked, holding bank accounts yet turning to alternative financial services such as money orders, check cashing, and payday loans. This TIAA Institute research brief explores who these retirees are, what services they use, and what their financial circumstances reveal about retirement security at the margins of mainstream finance.

Summary

Underbanked retirees are disproportionately younger, with 53% aged 60–69, suggesting some may be early or involuntary retirees who have not yet established stable income streams. The majority used only one type of alternative financial service in 2023, most commonly money orders and check cashing, though lower-income retirees were significantly more likely to use multiple services, including higher-cost options like payday and pawnshop loans. Two-thirds of underbanked retirees reported feeling financially okay, compared with 85% of fully banked retirees, and this gap widened sharply by income: 80% of higher-income underbanked retirees reported feeling okay financially, versus just 52% of their lower-income counterparts. The brief notes that without data on the frequency of AFS use, it remains difficult to distinguish between occasional reliance and chronic financial strain, and advocates for improved data collection to better identify and support retirees most at risk.

Key Insights

- Underbanked retirees skew lower-income and more racially diverse: 52% had household incomes under $50,000, and a combined 40% were Black or Hispanic, compared with 32% and 21% among all retirees, respectively.

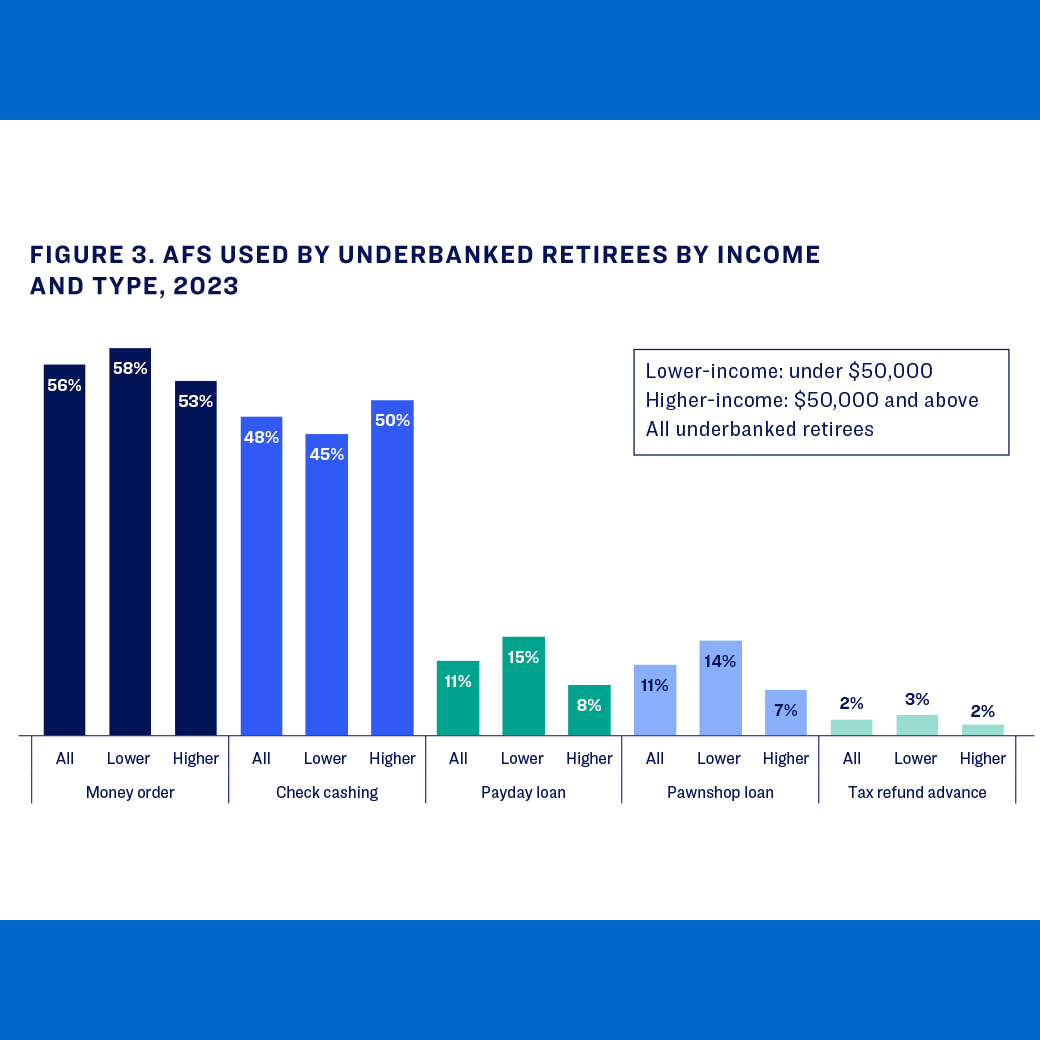

- Multiple AFS use signals compounded strain: 21% of lower-income underbanked retirees used more than one type of alternative financial service, compared with 13% of their higher-income counterparts.

- Savings and assets are strongly tied to perceived financial security: 76% of underbanked retirees with savings and assets reported feeling financially okay, versus just 31% of those without, a 45 percentage point gap.

- A small but vulnerable group faces concentrated risk: Approximately 1 million retirees, about 2% of all retirees, had lower incomes, used multiple AFS, and lacked savings and assets, representing meaningful financial strain.

- A critical data gap limits understanding: Current surveys do not capture how often retirees use AFS, making it impossible to distinguish sporadic use from chronic reliance, a distinction essential for designing effective interventions.