Employees and their families are increasingly responsible for their own financial security. At the same time, financial markets have become more complex, offering products that can be difficult to understand. Are Americans equipped to handle this new financial landscape?

Summary

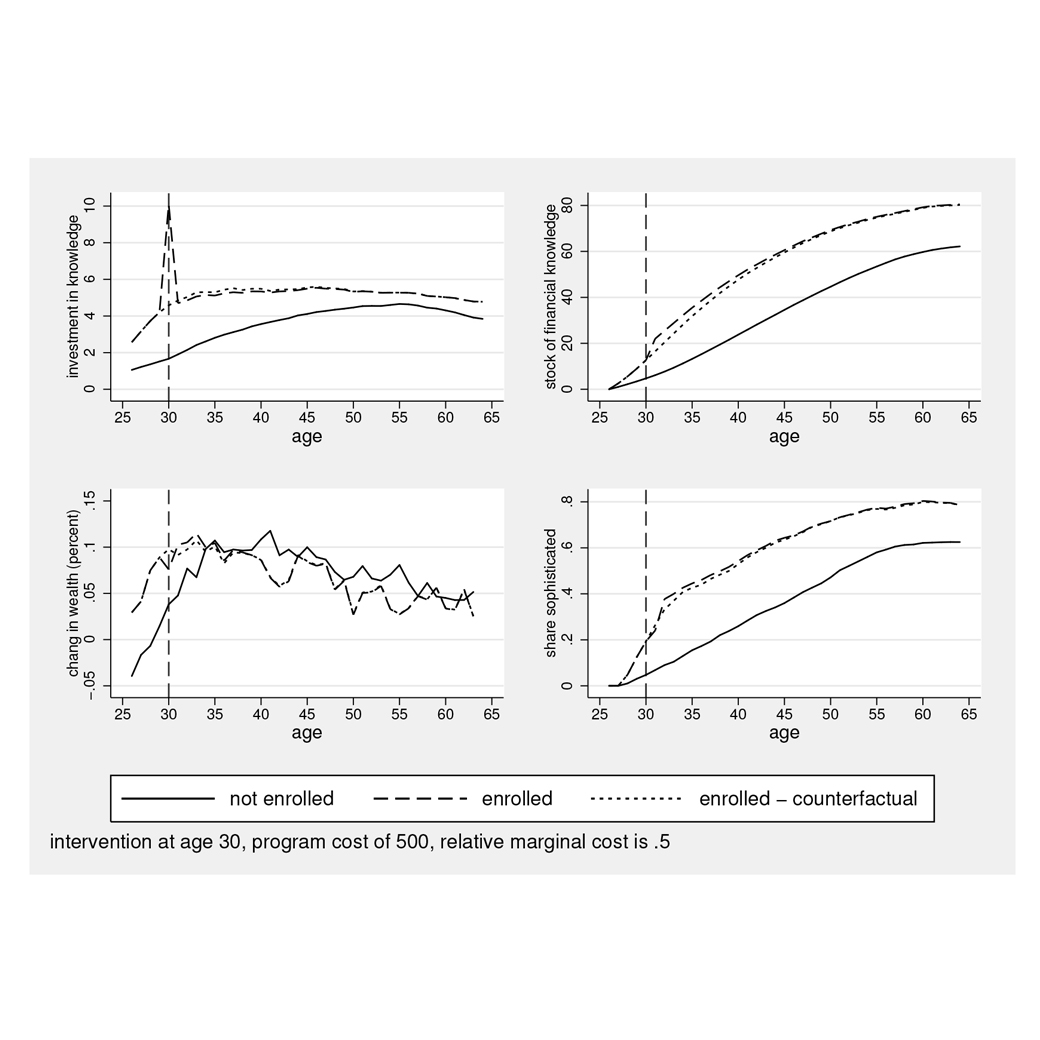

Prior research provides conflicting conclusions regarding the effectiveness of financial literacy programs, particularly those offered in the workplace. To explain such differences in evaluation and outcomes, this study uses conventional program evaluation econometric techniques and simulated data to account for selection and treatment effects.

Key Insights

- Studies show that large segments of the population are financially unsophisticated and do not understand simple interest, inflation and risk diversification.

- Given individual aptitudes, not everyone will benefit from financial education. Nevertheless, providing financial knowledge can be valuable, depending on when it is offered and what reinforcement is provided.

- Successful financial literacy programs provide follow-up outreach to reinforce learning; one-time programs tend to have little impact on retirement savings.

- People around the age of 40 generally show the greatest increase in knowledge following financial education.

- Targeting the right participants and providing reinforcement can raise savings at retirement by close to 10%.