While not a cure-all, increased financial literacy can lead to improved financial wellness among African Americans, even those with relatively low incomes.

Financial literacy, wellness and resilience among African Americans

Reports

New insights from the Personal Finance (P-Fin) Index

Introduction

The financial well-being of African Americans lags behind that of the U.S. population as a whole, and whites in particular. The reasons for this gap are complex, but one area of importance in addressing it is increased financial literacy.

Summary

Financial literacy is knowledge and understanding that enable sound financial decision making and effective management of personal finances. As such, improved financial literacy contributes to improved financial well-being. This report uses the third wave of the TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) to examine the state of financial literacy among African American adults and the relationship between financial literacy and financial wellness.

Key Insights

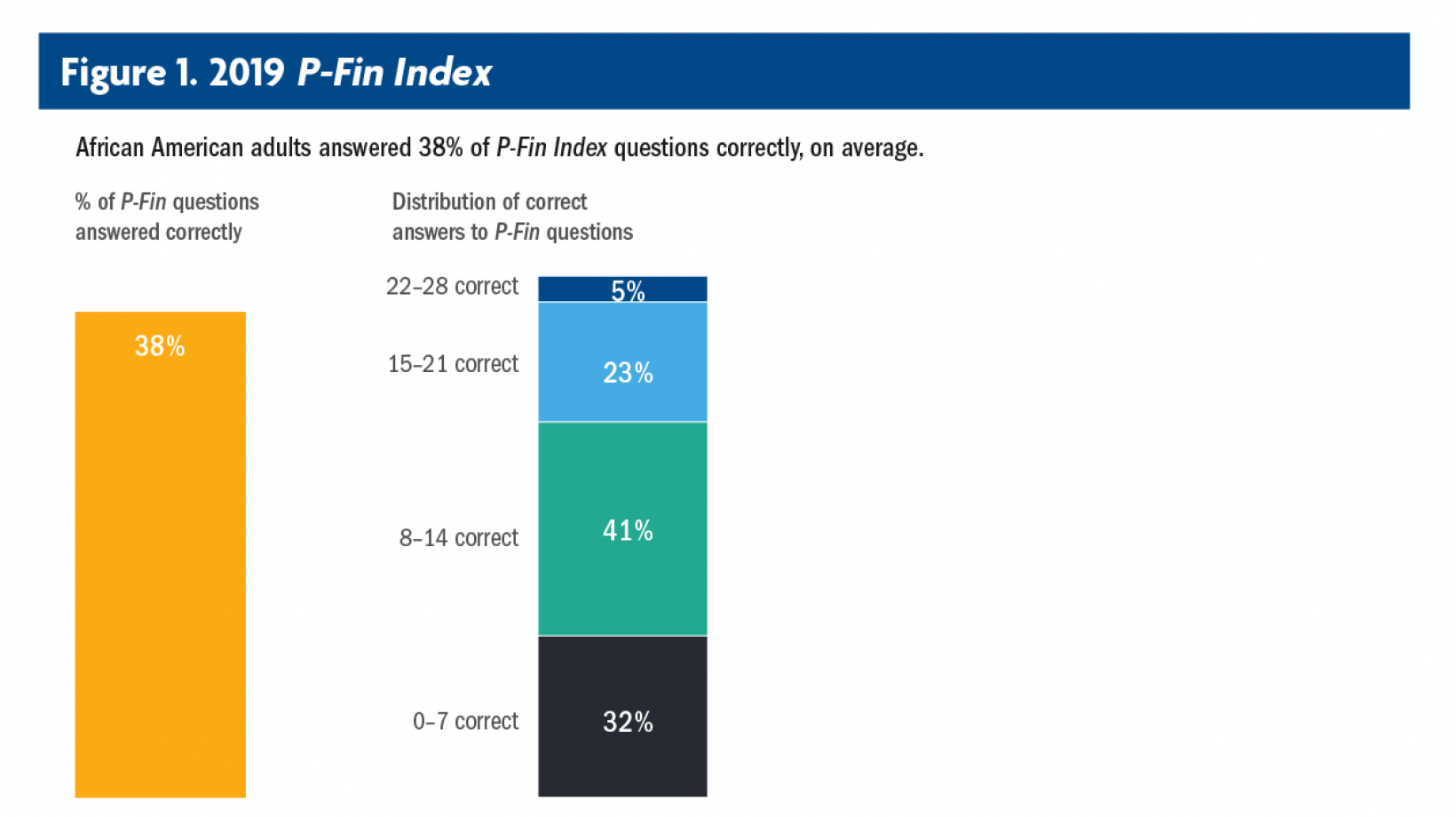

- On average, African Americans answered 38% of the P-Fin Index questions correctly; only 28% could correctly answer over half the questions.

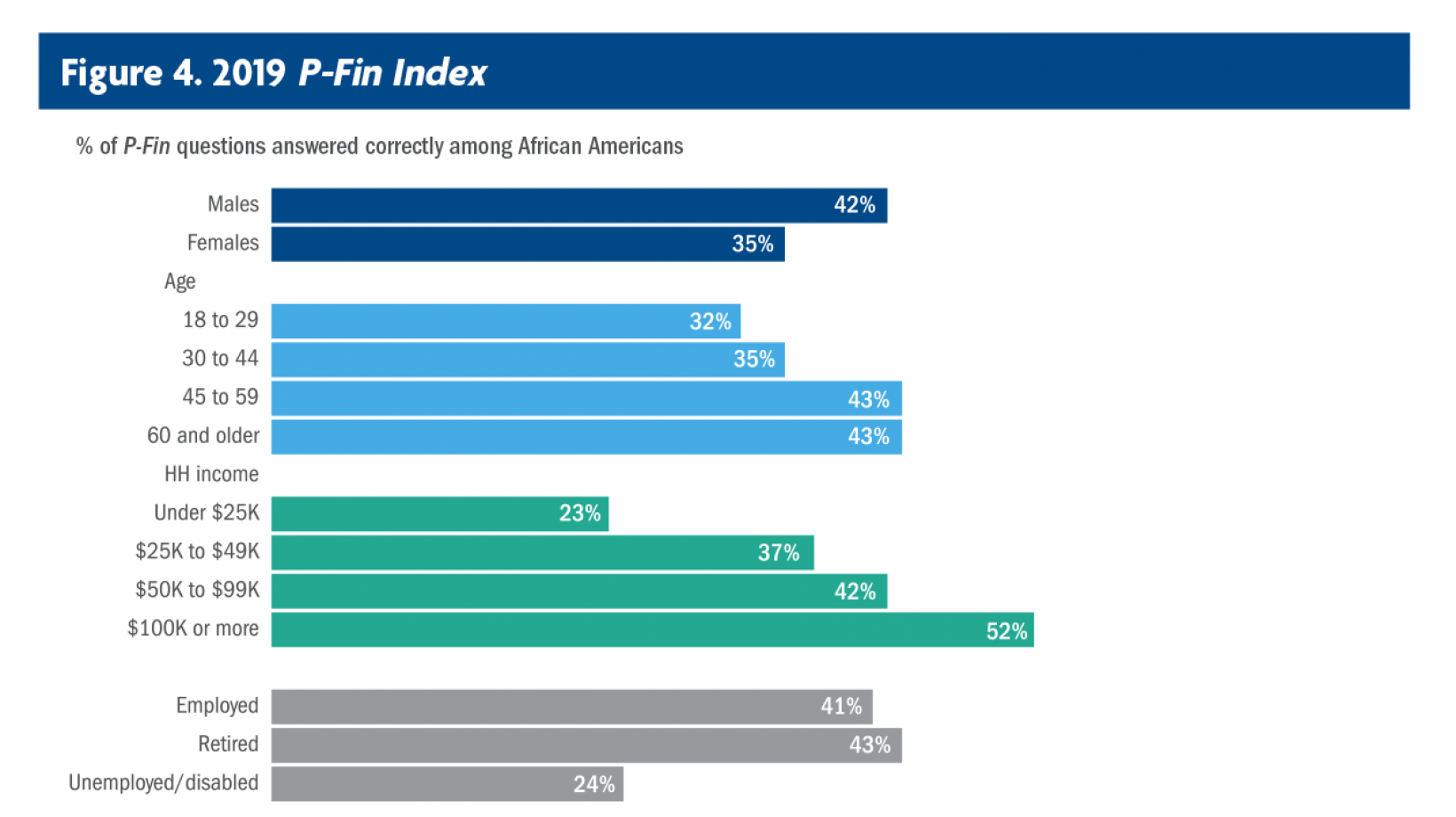

- Financial literacy within the African Americans community is greater among men, older individuals, those with more formal education, and those with higher incomes.

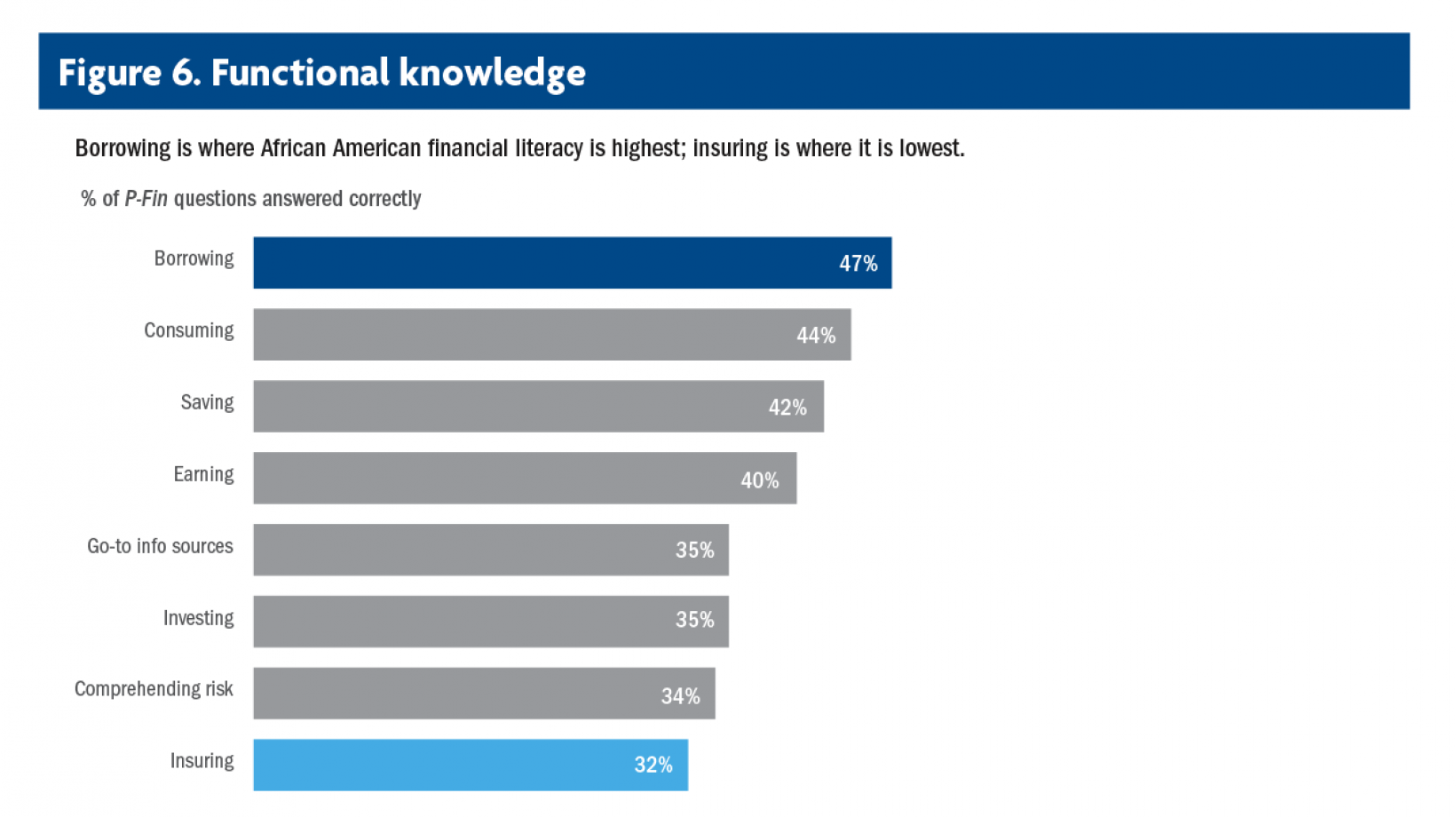

- “Insuring” is the least understood area of personal finance among African Americans, followed closely by “comprehending risk,” “investing,” and “identifying go-to information sources.”

- “Borrowing and debt management” is the area of highest personal finance knowledge among African Americans.

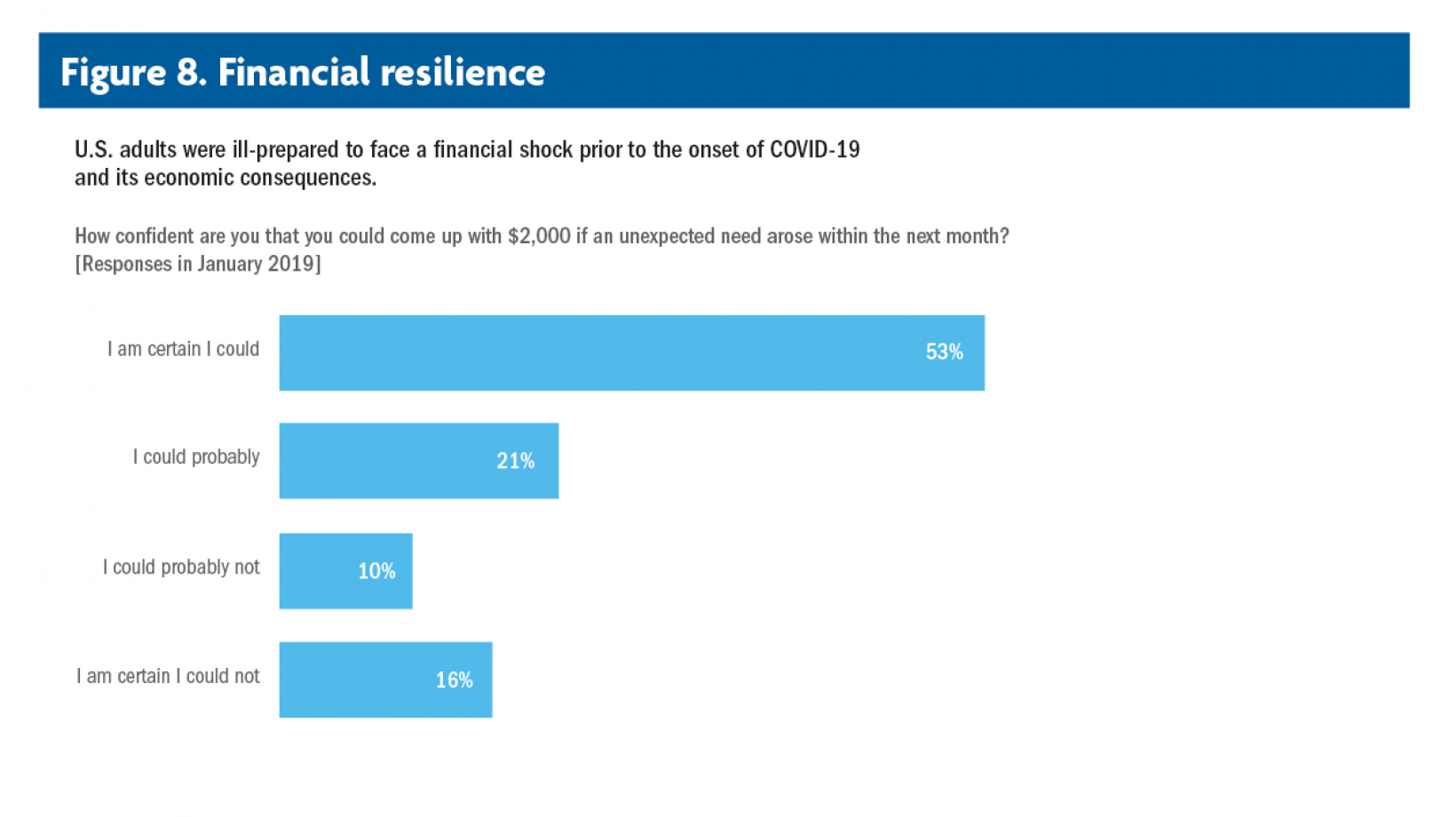

- A lack of financial resilience was more common among African Americans than whites in 2019, before the onset of COVID-19 and its economic consequences.

Methodology

The P-Fin Index is an online survey fielded each January with a sample of U.S. adults. The 2019 sample consists of 1,008 individuals. At each administration of the survey, the researchers oversample a particular demographic group to enable a detailed analysis of that group. In 2019, 1,015 African American adults were oversampled.

Explore Report Content

Executive Summary

The economic consequences of the COVID-19 pandemic have made obvious the precarious financial state of many American households. The capacity to cope with a financial shock is lacking, as is an understanding of fundamental personal finance concepts, such as risk and uncertainty, which is of particular importance during periods of economic turmoil.

Introduction

The financial situation of African Americans lags that of the U.S. population as a whole and of whites in particular. Simple economic indicators illustrate the gap. While 66% of African Americans report that they are doing at least OK financially, the comparable figure among whites is 78%. Median household income among African Americans was $35,400 in 2016; median household income of whites was $61,200. African American household net worth was $17,600 in 2016 and 19% had zero or negative net worth; the analogous figures for white households were $171,000 and 9%, respectively.

African American financial literacy

Financial literacy is low among many U.S. adults, including African Americans. On average, African American adults answered 38% of the P-Fin Index questions correctly. Only 28% answered over one-half of index questions correctly, with 5% answering over 75% correctly (Figure 1).

Demographic variations among African Americans

Financial literacy varies across demographic groups among African Americans (Figure 4). Observed variations in the average percentage of P-Fin Index questions answered correctly are consistent with those identified among the U.S. adult population as a whole.

READ MORE ABOUT DEMOGRAPHIC VARIATIONS AMONG AFRICAN AMERICANS

Personal finance functional knowledge

The P-Fin Index gauges personal finance knowledge and understanding in eight functional areas:

1. Earning—determinants of wages and take-home pay.

2. Consuming—budgets and managing spending.

3. Saving—factors that maximize accumulations.

4. Investing—investment types, risk and return.

5. Borrowing and managing debt—relationship between loan features and repayments.

6. Insuring—types of coverage and how insurance works.

7. Comprehending risk and uncertainty—understanding uncertain financial outcomes.

8. Go-to information sources—recognizing appropriate sources and advice.

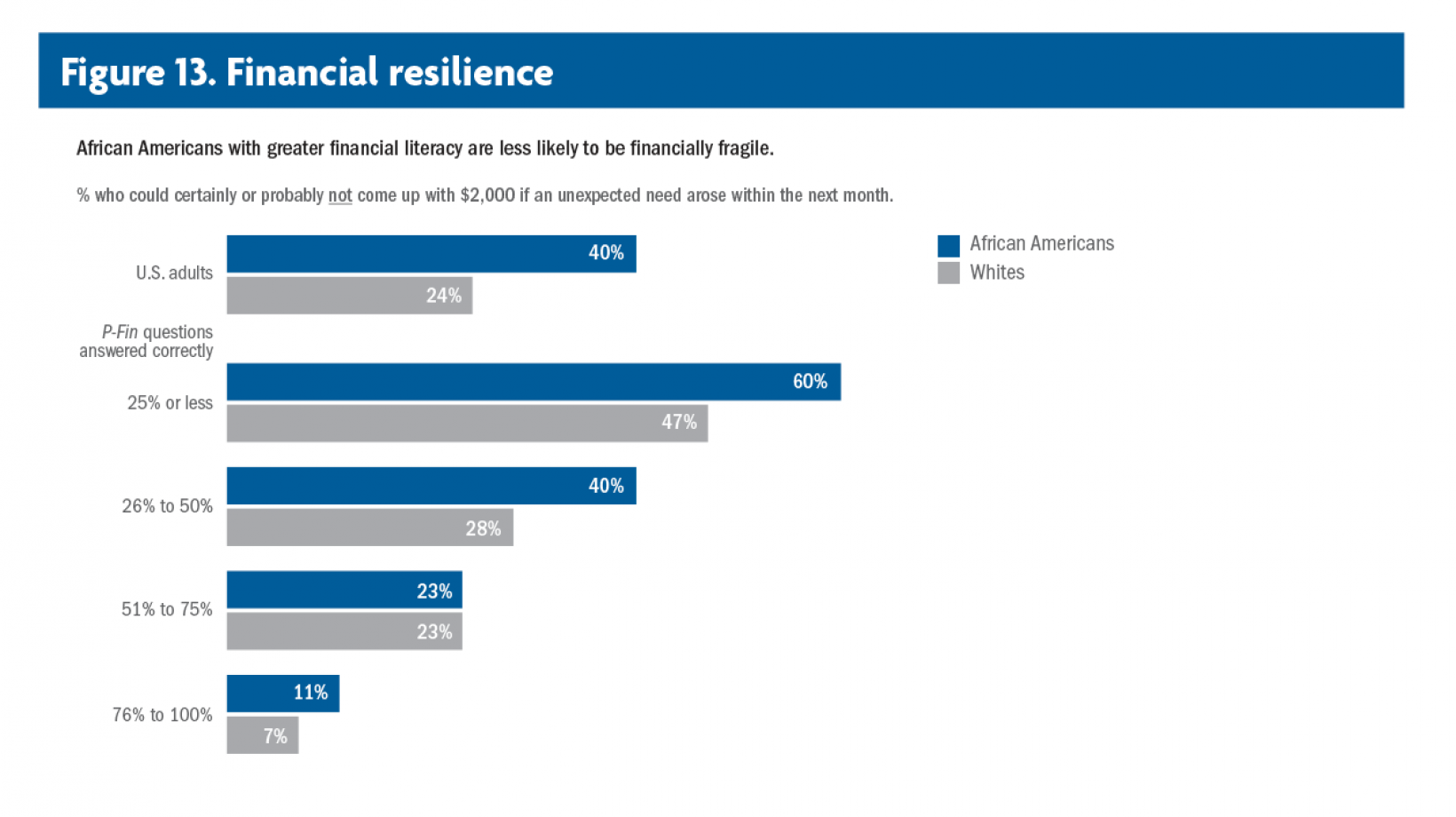

Financial resilience

Financial resilience is the ability to cope with an unexpected financial shock. Financial fragility is the inability to do so. 2019 P-Fin Index data, collected at a time of continued economic expansion prior to the onset of COVID-19, demonstrates how ill-positioned many Americans, including African Americans, were to face the economic consequences—furloughs or job loss, salary reductions, investment losses and unexpected expenses-of the pandemic.

Financial literacy and financial resilience

A strong relationship between financial literacy and financial resilience holds among both African Americans and whites. Among African Americans who correctly answered 25% or less of the P-Fin Index questions, 60% could certainly not or probably not come up with $2,000 within 30 days (Figure 13). This figure drops to only 11% among African Americans who correctly answered 75% or more of the index questions. In fact, at higher levels of financial literacy, financial resilience among African Americans and whites is equal (Figure 13). The link between financial literacy and financial resilience is verified in regression analysis (Table A1 of the Appendix). Among African Americans, there is a statistically significant relationship between financial literacy and financial resilience after controlling for various socioeconomic factors, such as education and household income. Those with greater financial literacy are more likely to have the capacity to handle a financial shock.

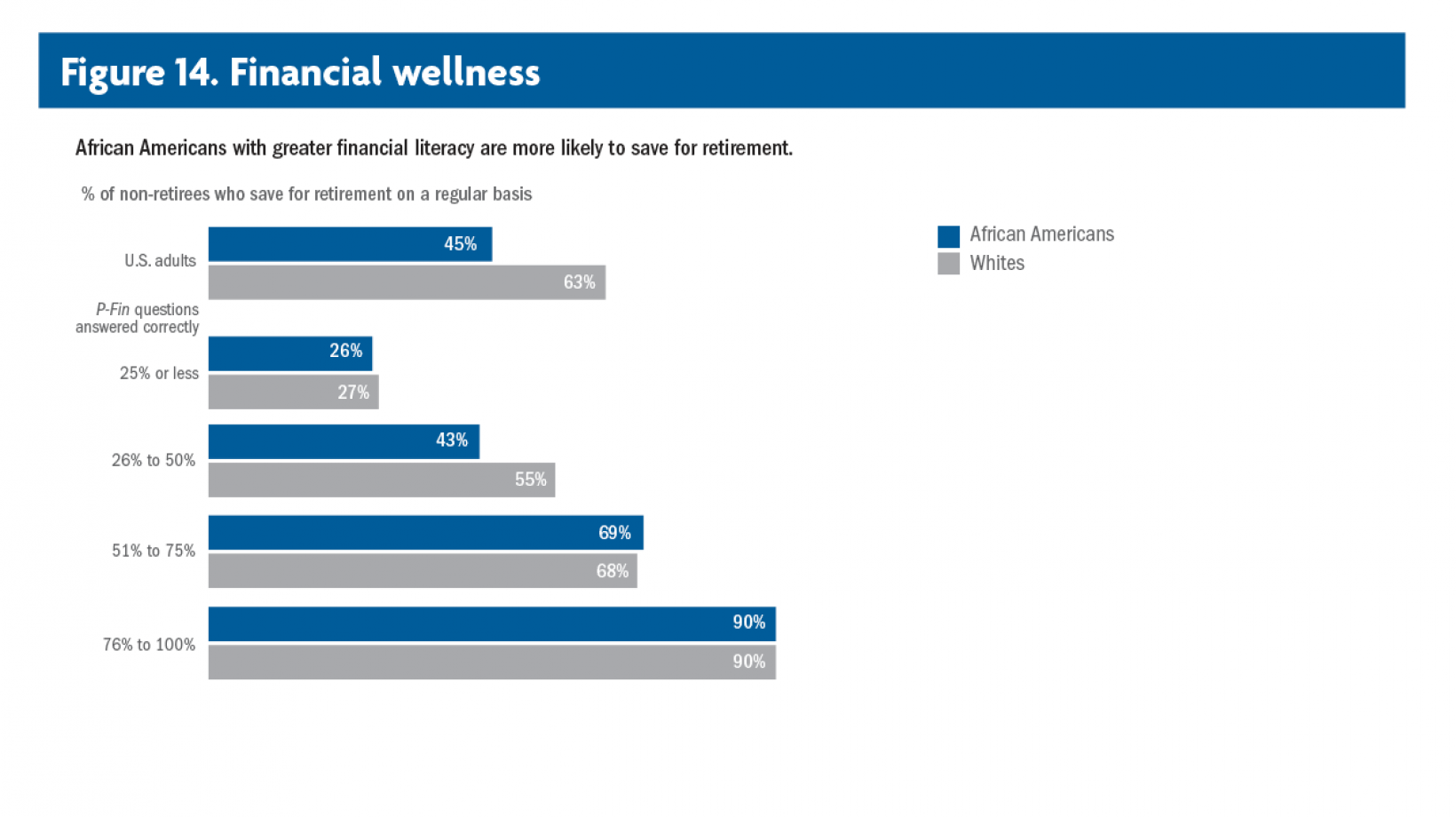

Financial wellness

Financial resilience is one indicator of financial wellness. The 2019 P-Fin Index survey contained several others—questions regarding behaviors that should promote financial wellness or regarding outcomes that demonstrate financial wellness:

- Saving and planning for retirement.

- Non-retirement savings.

- Debt constraint.

Discussion

Financial wellness depends in part on how well individuals navigate the myriad of financial decisions faced in the normal course of life. Financial literacy is knowledge and understanding that enable sound financial decision making and effective management of personal finances. As such, financial literacy contributes to financial well-being.

Authors

Paul Yakoboski

TIAA Institute

Annamaria Lusardi

GFLEC, The George Washington University

Andrea Hasler

GFLEC, The George Washington University