Planning and preparing for retirement, and subsequently living in retirement, should be grounded in expectations based on accurate information, as well as an understanding of the uncertainty involved.

Summary

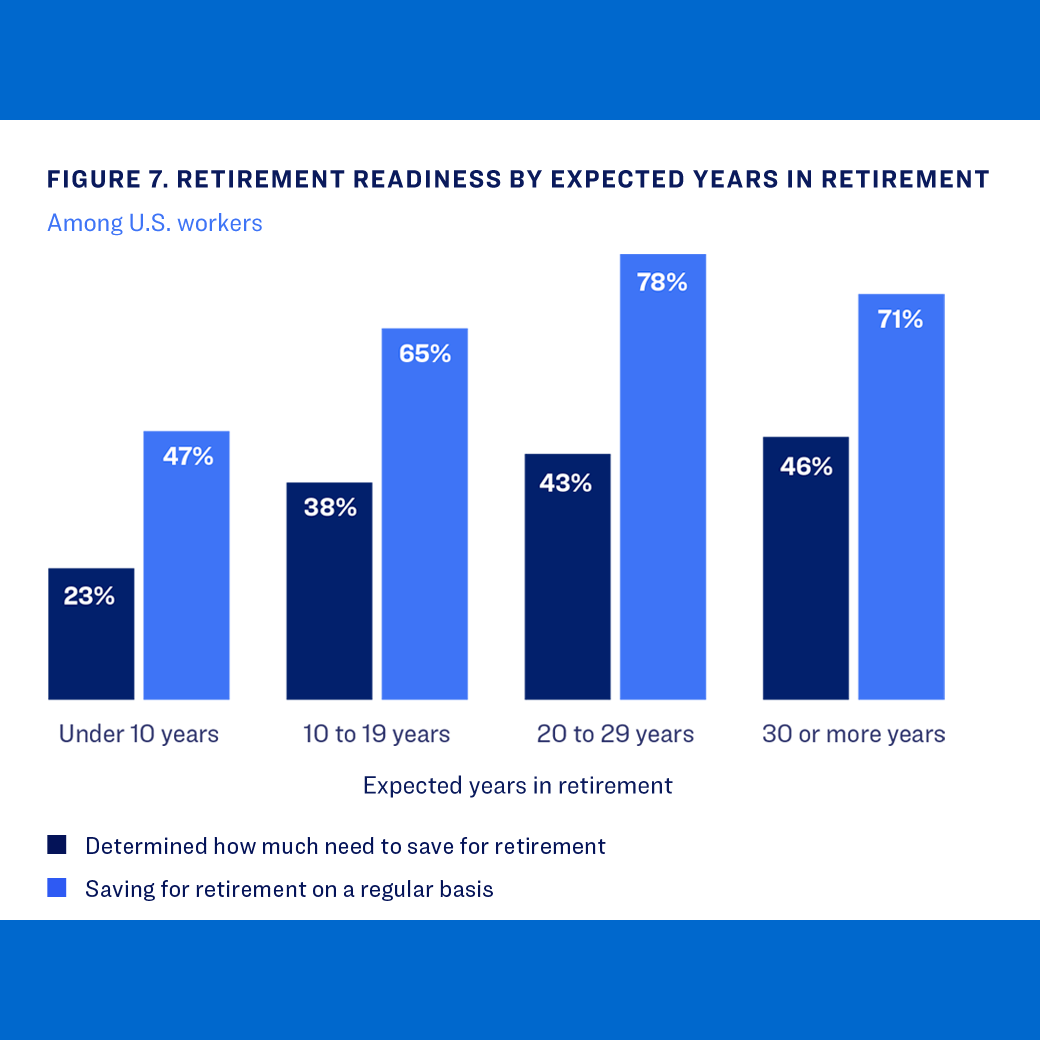

Uncertainty makes preparing for retirement challenging, particularly uncertainty about how long an individual will be retired. But workers have expectations about how long they’ll live and when they’ll retire, and these likely influence retirement-related decisions. This report examines these expectations, how they’re determined, and how they influence decision-making. Retirement plan sponsors and providers can use the resulting insights to help workers achieve retirement income security.

Key insights

- Longevity literacy tends to be poor among U.S. adults. Only 32% correctly answer a multiple-choice question asking like expectancy among 65-year-olds, while 35% underestimate it and 24% respond “don’t know.”

- Individuals’ perceptions of how long retirees live in general strongly influence their expectations about how long they will live in retirement. Seventy percent of those overestimating life expectancy for 65-year-olds anticipate living to at least age 90, while 74% of those underestimating age-65 life expectancy don’t expect to live to age 90.

- The influence of perception is problematic since poor longevity literacy is synonymous with misperceptions. Workers who expect relatively short lifespans due to misperceptions about population life expectancy are at risk of accumulating inadequate financial resources for retirement—their retirement planning horizon is “too short.”