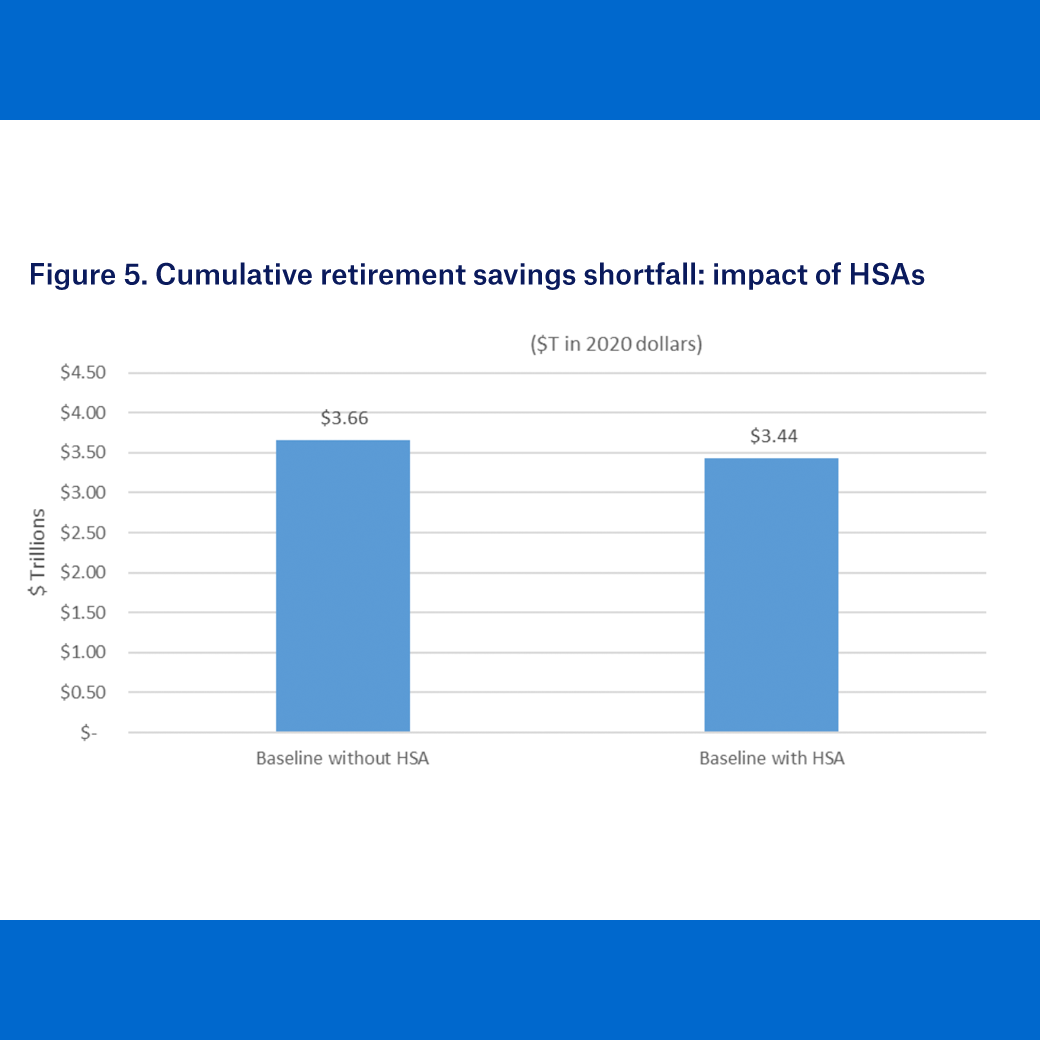

U.S. households are facing a $3.66 trillion aggregate retirement savings shortfall. How do health savings accounts (HSAs) affect retirement income adequacy?

Summary

Since retiree health care costs can be considerable, and Medicare was not designed to cover health care expenses in full, HSAs are often connected to retirement security. This study by the Employee Benefit Research Institute (EBRI) examines HSAs’ impact on retirement income adequacy under various conditions. The authors conclude that increasing access to HSAs and encouraging investment among HSA account holders can help reduce the cumulative retirement savings shortfall, particularly for demographic cohorts projected to face the largest deficits.

Key insights

- The aggregate retirement savings shortfall for all U.S. households ages 35–64 as of Dec. 31, 2020, was $3.66 trillion, excluding HSA adoption. The cumulative baseline deficit decreases by 6.2% to $3.44 trillion when status quo HSA utilization is considered.

- A strong improvement in HSA behavior increases retirement readiness by 7.4% to 64.7% retirement ready and reduces the baseline with HSA deficit by 15.0% to $2.92 trillion.

- The upper bounds of maxing out four HSA behavioral factors simultaneously increases retirement readiness rating by 36.0% to 81.9%, and reduces the baseline with HSA deficit by 74.5% to $0.88 trillion.

- Adoption of HSAs and subsequent improvements in behaviors have the most positive impact in absolute dollar terms on lower-income households and households led by women, Black/African Americans, and Hispanic Americans.

- Maximizing HSA enrollment accounts for more than half of the difference in the retirement saving shortfall relative to the baseline with HSA. Maximizing contribution and limiting distribution behavior have minor impacts.