While a number of published studies have measured how the number and mix of fund options influence investment patterns in retirement accounts few, if any, have examined how plan participants react to a large reduction in investment choices.

Summary

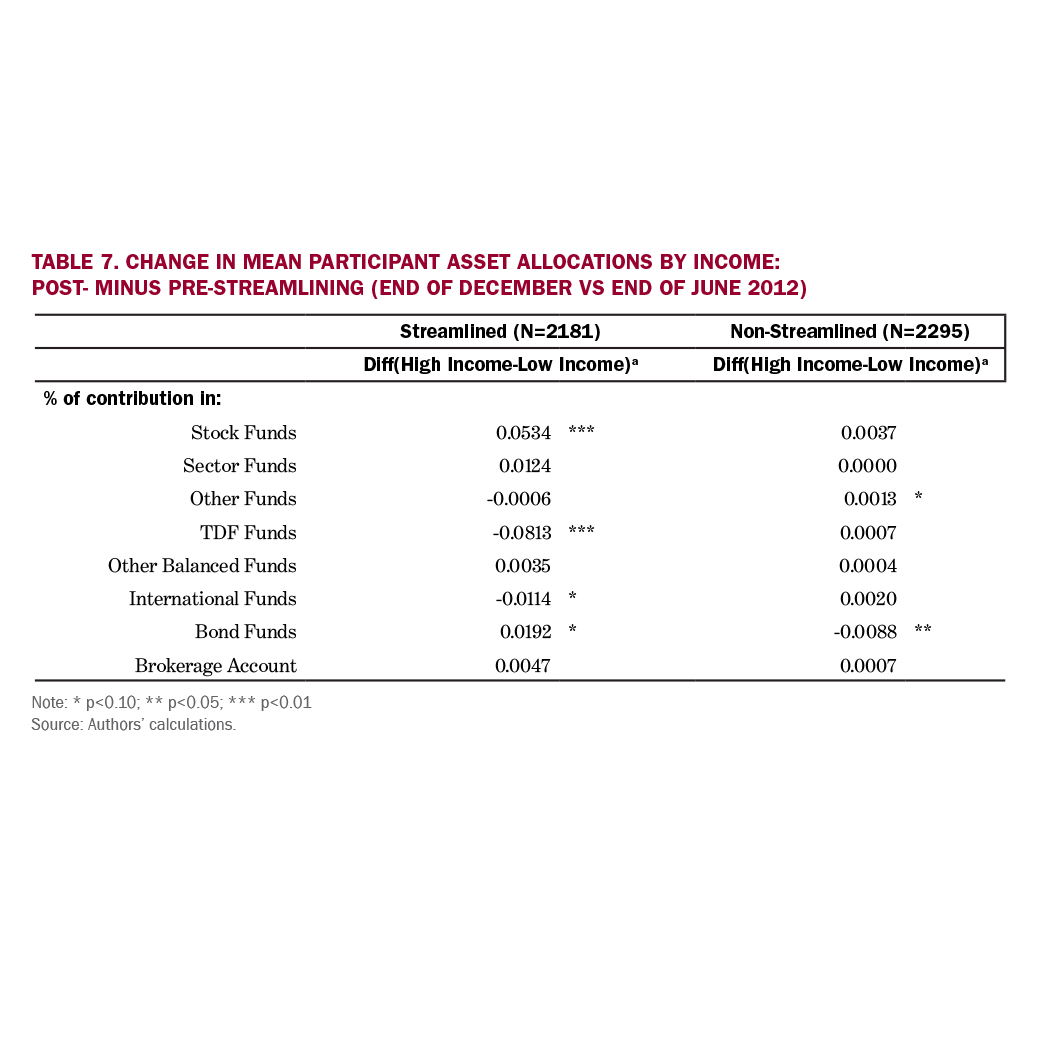

Recent research indicates too many retirement plan options can create confusion, resulting in poorly informed decisions. In June 2012, a large U.S. nonprofit institution eliminated nearly half of its defined contribution retirement plan’s investment options and grouped the remaining investments into four simple categories. The TIAA Institute commissioned a study examining how streamlined participants (i.e., holders of funds that were eliminated) altered their equity share, risk exposure, fees paid and turnover patterns given the new investment menu.

Key Insights

- Six months after the change, streamlined participants’ new investment allocations exhibited significantly lower turnover rates and expense ratios.

- The reductions were even greater for streamlined participants who were previously classified by the researchers as active traders.

- Based on reasonable assumptions, these reductions could lead to aggregate savings of $20.2 million for streamlined participants over a 20-year period, or in excess of $9,400 per participant.

- Streamlined participants’ portfolios also held significantly less equity and exhibited significantly lower risks due to reduced exposures to most systematic risk factors.

- The changes in portfolio characteristics largely remained intact 18 months after streamlining. Accordingly, the positive effects produced by the reform after the first six months were not undone by participant transactions over the subsequent 12 months.