Low financial literacy, especially with regards to risk and uncertainty, means that women are particularly ill-positioned to make appropriate financial decisions in the pandemic environment.

Financial literacy and wellness among U.S. women

Introduction

An ability to manage personal finances in periods of financial uncertainty and challenges depends, at least in part, on financial literacy.

Summary

Many Americans are functioning in today’s environment with a poor level of financial literacy. This is more true among women than men, and more true among underrepresented minority women than their white peers. Especially problematic in today’s environment is the finding that financial literacy is particularly low in the area of comprehending and understanding risk and uncertainty. On average, U.S. women correctly answered only one-third of the index questions related to risk and uncertainty. The same holds true among African American and Hispanic women. This means that individuals are ill-positioned to make decisions in a time when uncertainty and volatility dominate economic and financial life.

Key Insights

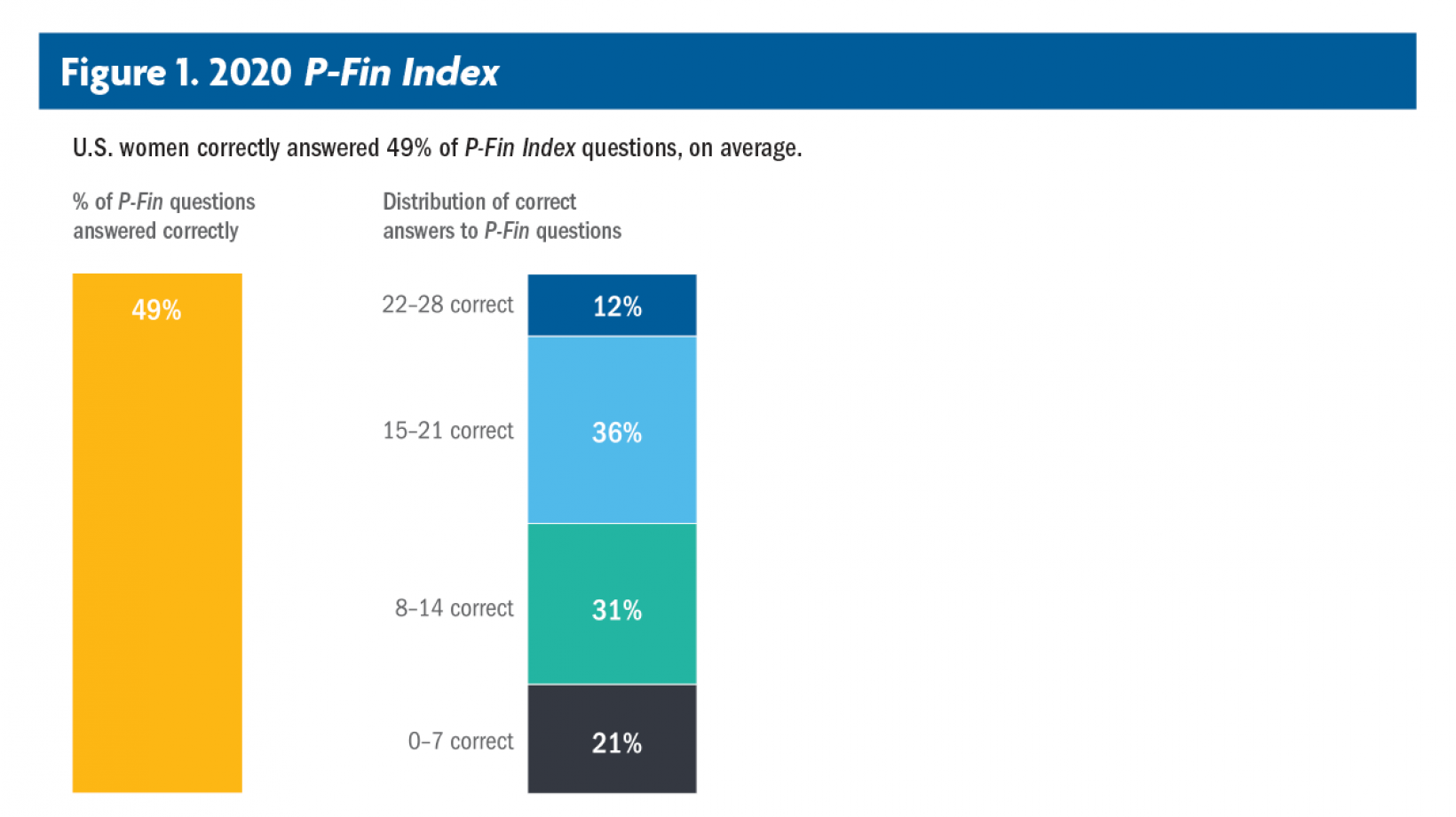

- On average, women correctly answered 49% of the 2020 P-Fin Index questions.

- Comprehending risk and uncertainty is the area of lowest financial literacy among women. Borrowing and debt management is their area of greatest personal finance knowledge.

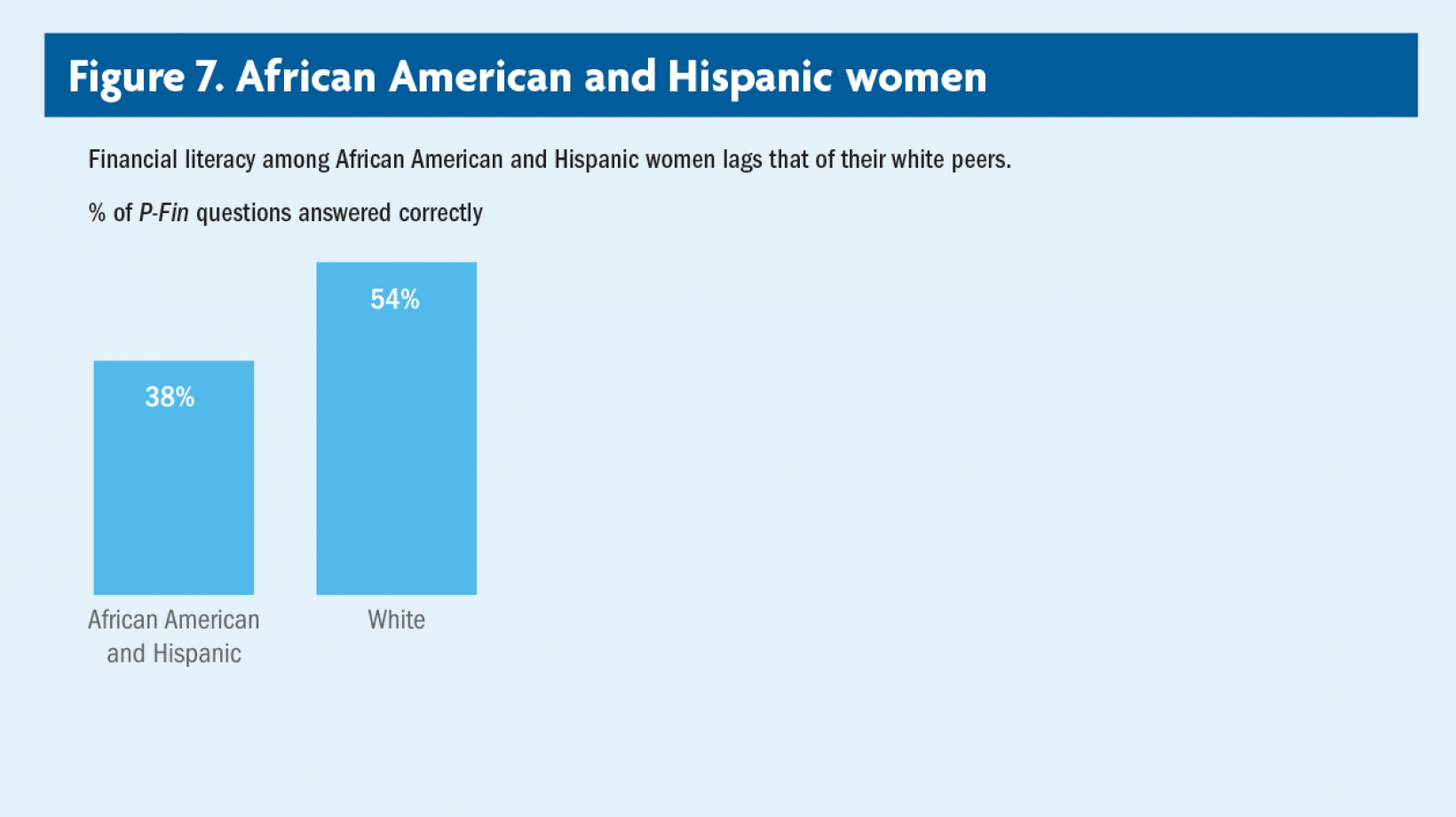

- Personal finance knowledge tends to be lower among underrepresented minority women—African American and Hispanic women—compared with their white peers. The former correctly answered 38% of the index questions, on average, and the latter 54%.

- Financial literacy is notably lower among underrepresented minority women compared with their white peers in seven of the eight functional areas. Comprehending risk is the lone area where functional knowledge is equal across the two groups.

- Greater financial literacy is associated with greater financial wellness among underrepresented minority women.

Explore Report Content

Executive summary

The TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) provides an annual measure of overall financial literacy among the U.S. adult population, plus a nuanced analysis of personal finance knowledge across eight functional areas. The 2020 P-Fin Index survey was fielded in January 2020 and included an oversample of women. This enables examining the state of financial literacy and financial wellness among U.S. women immediately before the onset of COVID-19. A more refined understanding of financial literacy among women, including areas of strength and weakness and variations among subgroups, can inform initiatives to improve financial wellness, particularly as the United States moves forward from the pandemic and its economic consequences.

Introduction

COVID-19 and its economic consequences have negatively affected the financial well-being of many Americans. For example, 30% of those employed in October 2019 have experienced a job loss or reduction in work hours since March 2020 (Board of Governors of the Federal Reserve System, 2020). Beyond the aggregate view, however, COVID-19 will exacerbate pre-existing gaps in financial well-being among U.S. adults to the extent that different demographic groups are disproportionately impacted. Women are at risk in this sense.

Women's financial literacy

Financial literacy is disturbingly low among U.S. adults in general, including women. On average, female adults correctly answered 49% of the 2020 P-Fin Index questions. Forty-eight percent correctly answered over one-half of the index questions, with 12% demonstrating a relatively high level of financial literacy, i.e., they answered over 75% correctly (Figure

Self-perceptions

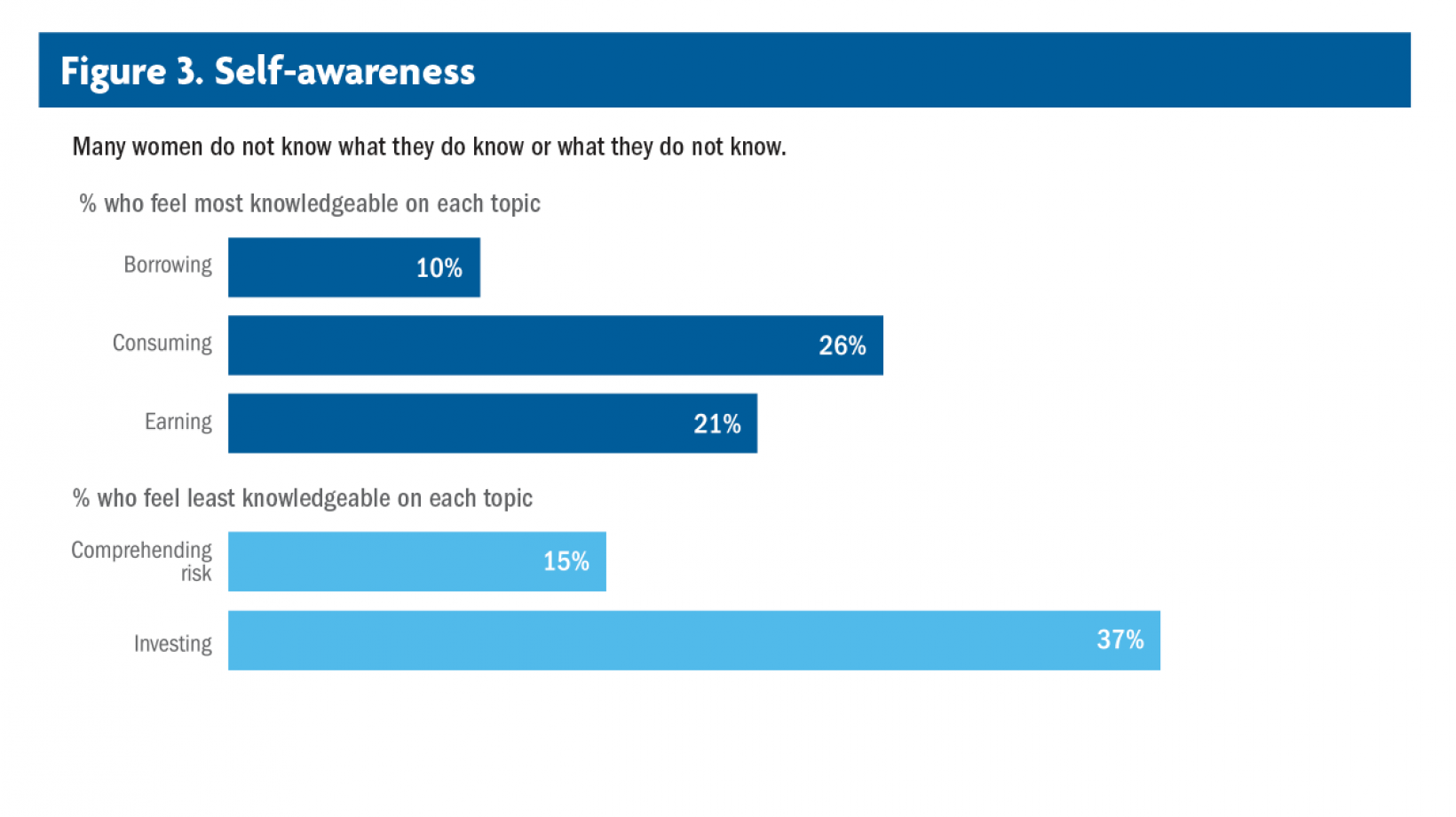

Many women do not know what they do know in terms of financial literacy. Consuming and earning are the areas where the largest share of women rate their financial knowledge as being highest (26% and 21%, respectively) (Figure 3). While these are areas of relative strength in terms of financial literacy, clearly many do not recognize the level of knowledge they possess regarding borrowing. While borrowing is where functional knowledge is greatest among women, only 10% rate themselves most knowledgeable in this area. Perhaps challenges individuals face in managing debt are viewed as signaling a lack of knowledge.

Variations among women

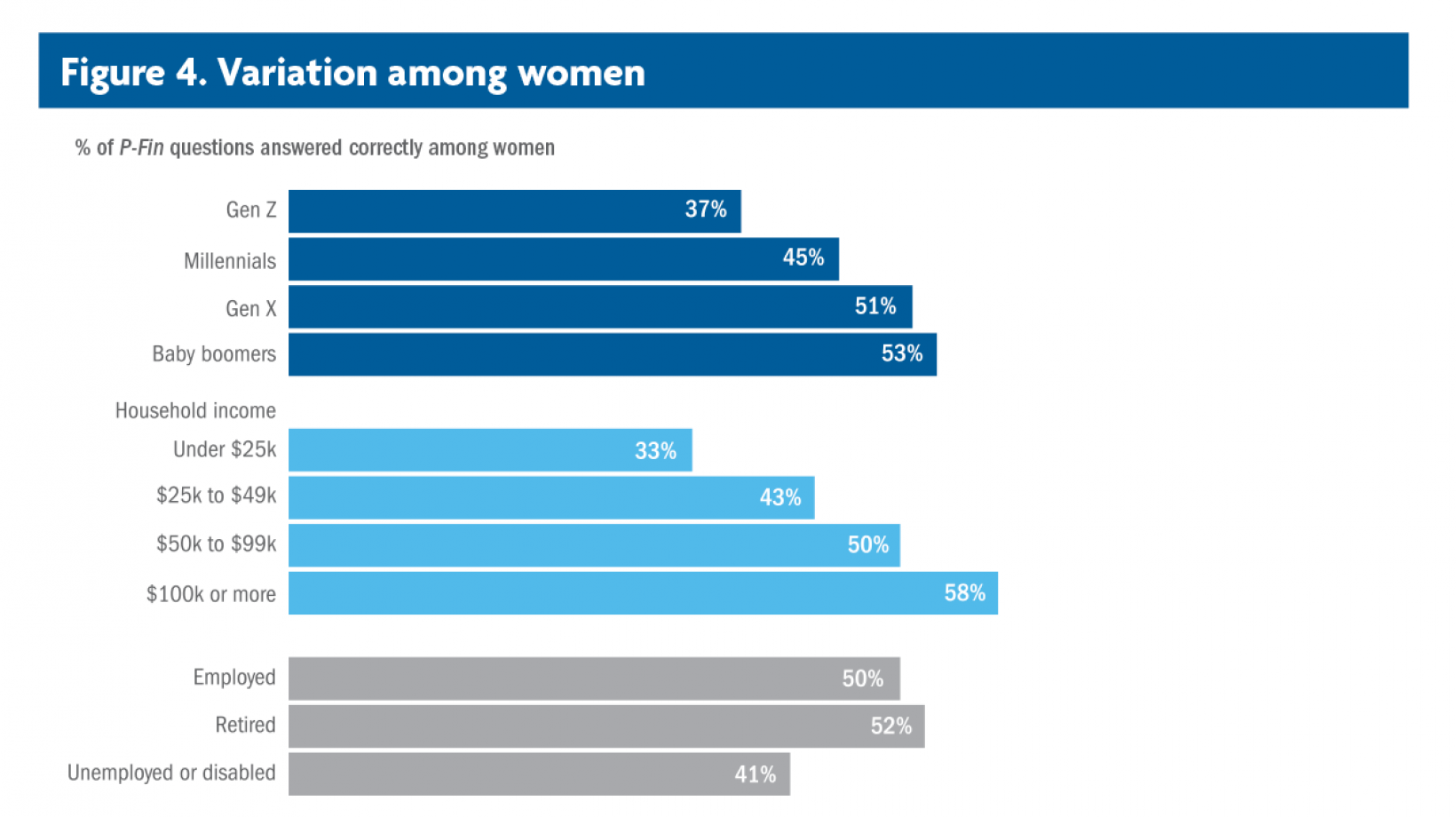

Financial literacy among women varies across socioeconomic and demographic groups (Figure 4).

- Financial literacy tends to be lowest among Gen Z women and highest among Gen X and baby boomers. Gen Z correctly answered 37% of the index questions, on average, compared with 51% among Gen X and 53% among boomers. While generation and age effects cannot be distinguished in a single cross-section of data, these findings stand out for how little young women seem to know given the complexity of today’s financial environment.

Financial literacy among underrepresented minority women

Personal finance knowledge tends to be lower among underrepresented minority women—African American and Hispanic women—compared with their white peers. The former correctly answered 38% of the index questions, on average, and the latter 54% (Figure 7). This is analogous to financial literacy levels among the entire U.S. adult population—underrepresented minorities correctly answered 38% of the index questions, on average, while their white peers correctly answered 58%.

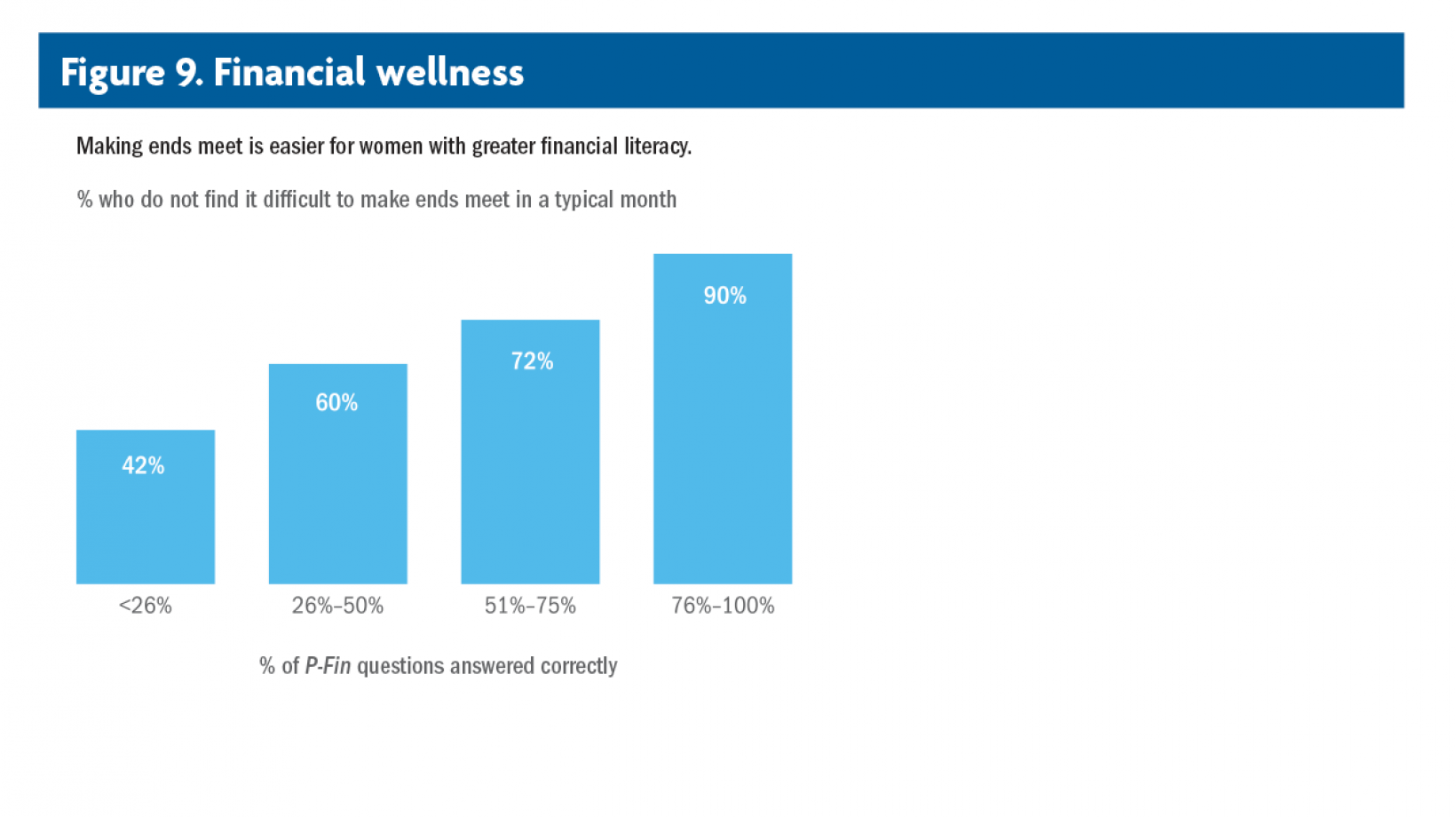

Financial wellness

Previous P-Fin Index findings have demonstrated that financial wellness tends to be greater among U.S. adults with higher levels of financial literacy.11 This implies that those with greater financial literacy are better positioned along various dimensions to weather adverse economic conditions such as those that exist today.

The same finding holds when focusing on women in particular—those with greater financial literacy tend to exhibit greater financial wellness.

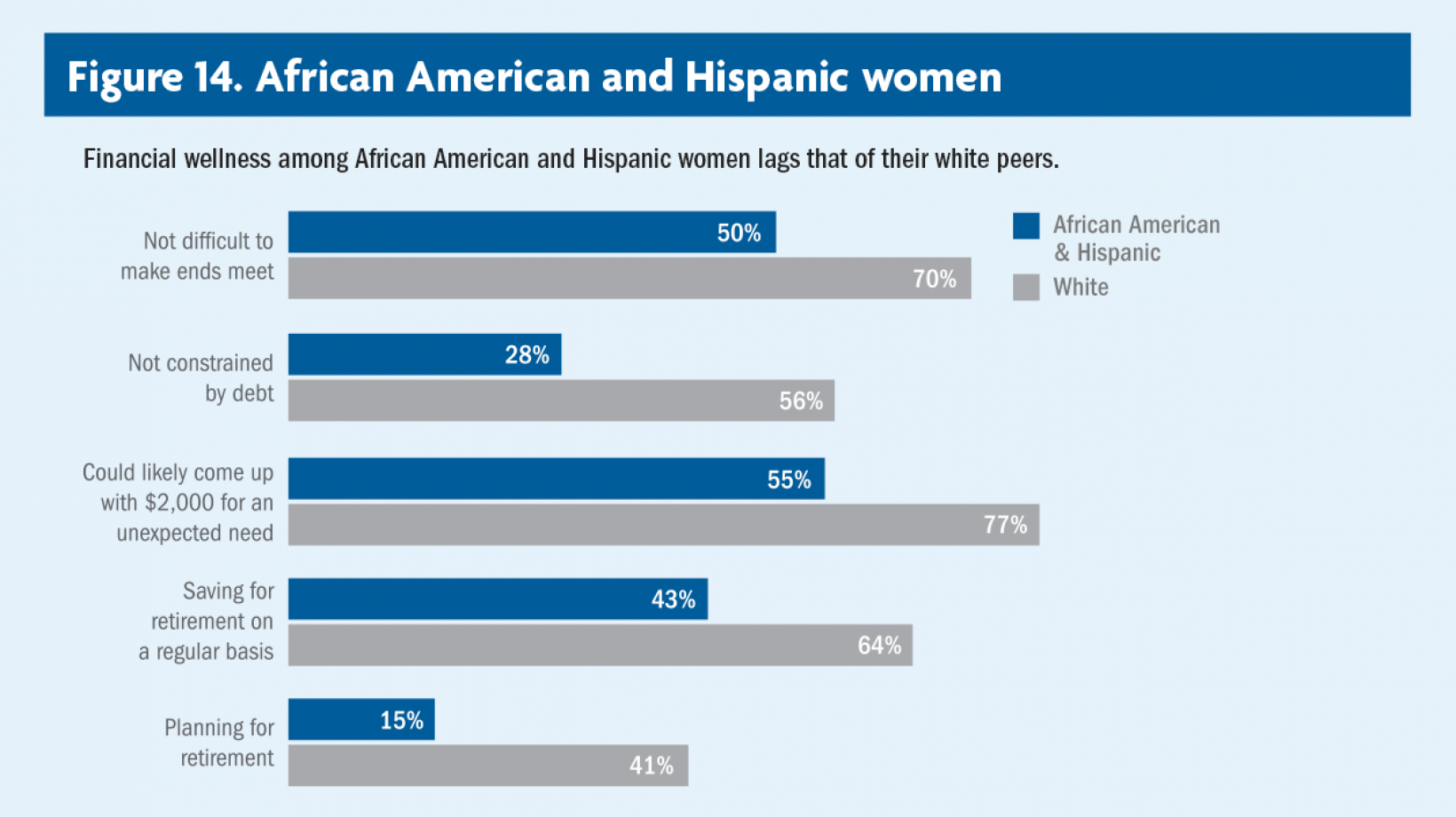

Financial wellness among underrepresented minority women

For each indicator of financial wellness in the P-Fin Index survey, there is a significant gap between underrepresented minority women and their white peers (Figure 14).

The gender gap

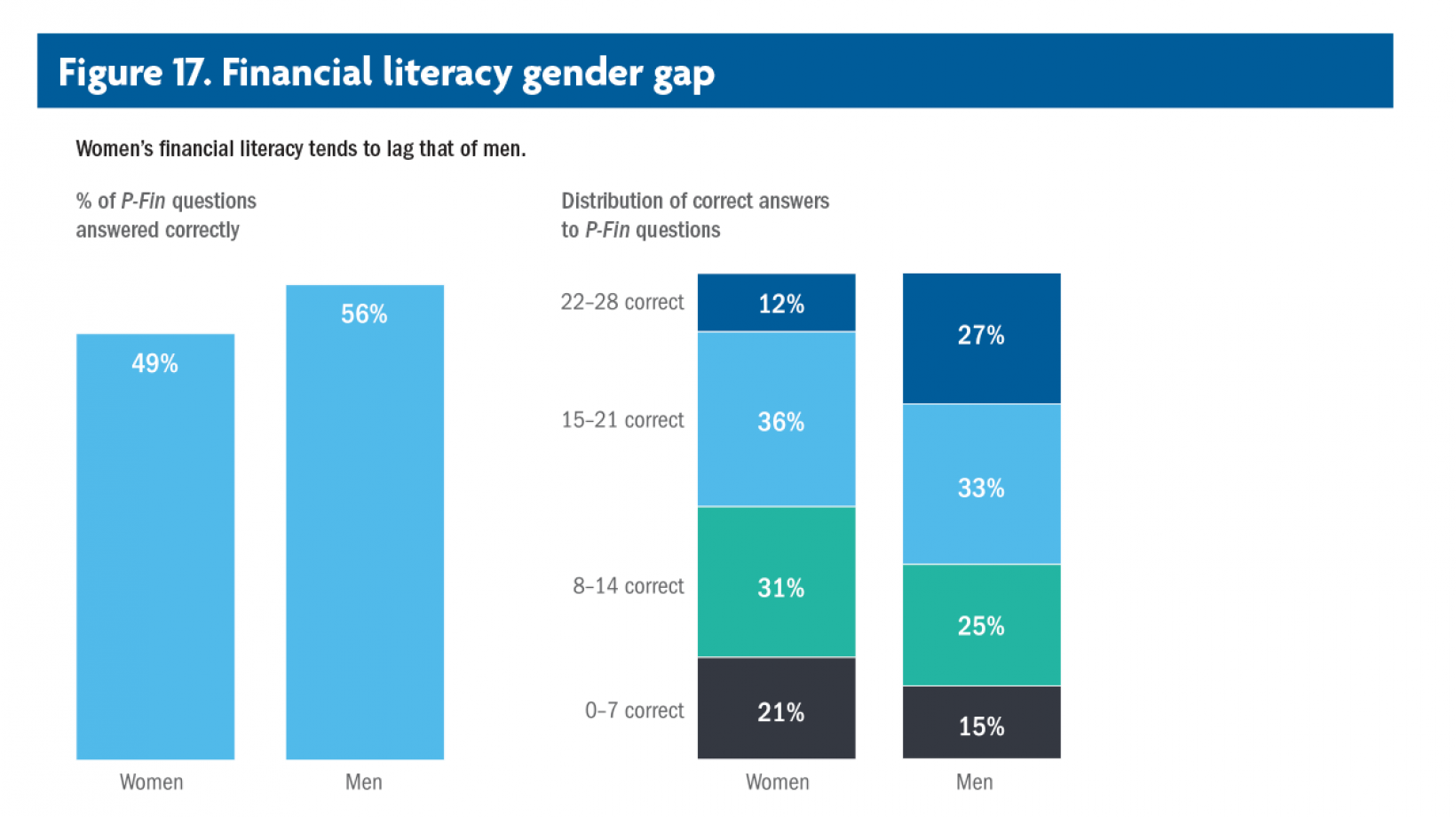

Comparing financial literacy among women with men provides context useful in tailoring financial literacy initiatives to the particular needs of women. As expected, personal finance knowledge tends to be lower among women than among men. On average, men correctly answered 56% of the P-Fin Index questions (Figure 17). Sixty percent of men correctly answered over one-half of the index questions, with 27% answering over 75% correctly. In contrast, 21% of women demonstrated a relatively low level of financial literacy, i.e., they correctly answered 25% or less of the index questions, compared with 15% of men.

Discussion

Financial literacy is knowledge and understanding that enable sound financial decision making and effective management of personal finances. In times that are anything but normal—like today with the COVID-19 pandemic and its severe economic consequences—the ability to make appropriate financial decisions matters greatly.

Download Financial Literacy and Wellness Amount U.S. WomenOpens pdf

Authors

Paul Yakoboski

TIAA Institute

Annamaria Lusardi

GFLEC, The George Washington University

Andrea Hasler

GFLEC, The George Washington University